My partner in travelling reached 66 years of age recently. He is fortunate to get his state pension at this age, along with his workplace pensions and his bus pass! This birthday was a huge milestone for us on our journey from being economically inactive to becoming pensioners.

When we both stopped working the nine to five in 2017 we had little income to speak of. What we did have was a spreadsheet [of course] with nine columns, one for each year until 2025. The spreadsheet forecast how much of our savings we would need to spend every year so that we could pay the bills and live our lives. We reviewed it regularly in the light of the actual amount we had spent and how much I had managed to earn as a travel writer. Every year on the 31 December I cheerfully deleted the column for the year that had ended. As our pensions have crept closer the trusty spreadsheet has diminished.

I met an old friend I hadn’t seen for a few years recently and she asked me, ‘Did the spreadsheet work?’ Her question made me smile; feel grateful that she had remembered all those conversations about early retirement we had; and also stop and think before I answered her. I realised, yes, the spreadsheet had worked and so much better than I might have hoped.

The spreadsheet started life in 2011 and until 2017 was used to track how much more money we needed to save until we could afford to retire. As the pennies became pounds the amount we needed before we could stop work got smaller.

From 2017 the spreadsheet’s use changed and a new section was added for cashflow, so that we never tied up any money long-term that we needed as our ‘income’ in the short-term. In constant use, the spreadsheet keeps us on track month by month as the details of our spending [mostly in our control and predictable] and income [unpredictable until my small NHS pension arrived in 2020] were updated. This enabled us to see at almost a glance what fiscal flexibility we had every year. Without this information, making financial decisions that were outside our budget would have been more difficult. In particular, the spreadsheet informed our decision to move house in 2019 [something we hadn’t planned for in 2017]. The spreadsheet has been our companion on our journey, growing and evolving as our life has changed, always helpful, sometimes accommodating and never draconian.

It has held my hand for so long, I have realised I will miss this spreadsheet when all the columns have been deleted in two years time. In 2026 all our pensions will have matured, I will also have a bus pass and we will have two fairly predictable incomes once again. Although we won’t be part of the workforce it will feel like we have gone back in time to the days of straightforward fixed incomes. Making sure our expenditure stays within budget will be managed by a different [and even older] spreadsheet!

I never guessed I was the sort of person who would become sentimental about a spreadsheet. Maybe it isn’t surprising when I consider how much it is a symbol of the big step we made in giving up our jobs in 2017. I think maybe my old friend would understand my emotions and I hope you readers do too.

A recent article in the i newspaper [link at the end] tells readers a couple will need £34,000 a year to have a moderate retirement. The piece refers to former pensions minister Steve Webb and includes tips for making the most of your money. It suggest three levels of retirement income that you could aim to save for; basic; moderate and comfortable. Our budget of £27,000 a year fell somewhere between basic and moderate!

As I have written before, I thnk that everyone has different spending habits and priorities and no one person’s retirement will be the same as another but here was an article confidently prescribing the income you need for retirement. I wondered how they could be so precise.

The article states:

A moderate retirement – which gives you two weeks’ holiday in Europe and a long weekend every year, as well as money to maintain your home and £800 to spend annually on clothes – costs around £23,000 if you are single, and £34,000 if you are a couple (these figures assume you have paid off your mortgage).

By Jessie Hewitson i News Money and Business Editor March 4, 2023

Frustatingly, the article doesn’t give much detail about how a retirees money would be spent so it is hard to understand the working out. Regular blog readers will know that we have quite a lot more holidays than the two weeks and long weekend the piece allow for. Even with only £27,000/year to play with we are usually away for over three months each year! The article suggests we are doing the impossible.

The clothing allowance of £800 per year is mentioned and it is implied that this amount is per person, budgeting £1,600 for a retired couple to spend on clothes. For the last couple of years we have spent between £600 and £700 on clothes for the two of us, quite a significant saving. Maybe with a full breakdown I would be able to see where else we spend less than this average moderate retired couple.

For a while my mind wandered as I tried to imagine how one person would spend £800 on clothes. I found my imagination just isn’t that good and I sought help from the John Lewis website. Some browsing revealed that you could spend £100 on a pair of jeans, not much more than I would spend on a pair of hiking trousers. These jeans [like my hiking trousers] would no doubt last years so doesn’t really explain the £800 per person. Ramping things up, I began looking at winter coats, sorting them by the highest price. Apparently you can spend over £1,000 on a coat! That is expensive but surely for that price it would last a lifetime! All this pointless browsing just proves that everyone’s retirement is different. There will be people who enjoy buying and wearing expensive clothes but I am not one of them.

Our clothing policy is that things are replaced when they wear out. If something doesn’t get worn during a year it goes to the charity shop with the exception of my back-of-a-drawer guilt clothing. I admit I own a couple of items that I never [or hardly ever] wear. I still have the frock I wore at my graduation in 1995 even though I haven’t worn it for years. I was so proud of my achievement when I wore my cap and gown [and this dress] at the graduation ceremony. I earned my degree at the age of 35 and the dress is still tied in with those memories and I haven’t been able to give it away.

Anyway, I have digressed. Back to retirement. Given that the article budgets so much for clothing it would be good to scrutinise other spending lines to see if they stand up to scrutiny. Without the detail I can only guess that the holidays are more luxurious than ours, more expensive supermarkets are used for shopping and maybe decorators and new curtains are allowed for rather than DIY and second hand.

How much income you need in retirement is a common and legitimate question and despite my critique, the article does contain some useful advice for anyone planning their retirement so please read it. What it doesn’t say is that the only way to know how much YOU will need in retirement is to monitor your own spending, rather than relying on someone else’s estimate. Once you have a handle on how much you spend and what you buy, you can begin to estimate what you need. It might be £34,000 or it might be less or more. Only you will know if your own retirement essential is watching a new film at the cinema every week, gym membership, drinking a glass of high-quality wine every evening or maybe all or none of these things. Mapping out your spending and planning accordingly will help you have the retirement you want. You certainly don’t have to spend £800 a year on new clothes but if that is your priority then budget for it.

The cost of living has been on everyone’s minds in 2022 so how did we cope in a year where inflation raced ahead into double figures, while interest on savings lagged behind? Did we make any changes to our lives that show up in our spending? Once again I have divulged the expenditure of a couple living in the northwest of England in all its peculiarity and shortcomings.

During 2022 we still only had my small NHS pension, my irregular travel writer income, interest and Premium Bond winnings [no we didn’t win big!] to pad out our savings. This income contributes about 40% of our spending and it is our dwindling savings that provide the majority of our funds through the year. We are beyond excited that in 2023 one of Anthony’s work-related pensions kicks in [over 20 years of service] as we gradually come to the end of our savings.

When we retired in 2017 we aimed to live on less than £27,000 a year for the foreseeable future, and despite high inflation we have spent under that figure for five of the last six years but it was a close run thing in 2022. Today the average household in the UK spends just over £30,000 a year [even if you take out mortgage / rent costs] and if we were both earning minimum wage for a 37 hour week and paying tax we would have an income of almost £33,000, so we were not budgetting for anything like the lap of luxury.

As in previous years, expensive home improvements that we consider one-off are kept separate and not part of the headline figure. On top of the budgeted expenditure in the usual categories [see below], in 2022 we also eventually managed to renovate our tired bathroom, splashing out £10,000 on a new super-modern bathroom and flooring for our hallway. I am hopeful I will never have to re-fit a bathroom again [I’ve no idea how anyone manages this without a campervan to fall back on] and I hope this one will see me out!

Here is how our budget breaks down into my different categories:

Essentials – total £8,941 [33% of total spending] [2021 £8,730 / 38%]

Food – £4,074 [2021 £4,142] – I have watched this figure carefully throughout the year and I am surprised it is less than 2021! The evidence suggests that the price of food has increased and there was a point where a pack of butter seemed to increase by the day and yet the spreadsheet doesn’t lie. I can’t explain this and my waistline would suggest we haven’t starved. We continue being vegetarian and using Lidl for most of our shopping, with top ups at the Co-op, Sainsburys and Tesco. We were in Germany and the Netherlands for two months of the year but food seemed a similar price there and we have averaged £339 / month spending in supermarkets [including alcohol] in 2022.

Utilities, insurance & service charges for a 2-bed 57.2 sq mtrs [615.7 sq feet] bungalow – £4,031 [2021 £3,854] – Considering the rising cost of everything, this budget line hasn’t risen too much either. Like most other people we have received the government help on our energy bills. We can’t do much about our Council Tax and TV License but did get a better deal on our home broadband. We have always saved energy and water for our pockets and the environment, using grey water to flush the loo, switching the shower off while we lather up and only washing clothes at 30C.

Our health – £836 [2021 £734] – Most of this spending in 2022 is on physiotherapy after my ongoing bout of sciatic pain. The NHS waiting list for physiotherapy is generally so long we just get on with this ourselves to prevent problems becoming chronic. This is certainly a frugal fail as after paying £55 a session for two months I found out our GP practice has two NHS physiotherapists with waiting lists of only a few weeks!

The money we spend on the essentials above are, in theory, the minimum we need to survive, if nothing goes wrong or wears out and we didn’t own a campervan and never went anywhere!

Stuff (electronics, books, newspapers and other kit) – £4,719 [18% of total spending] [2021 £3,170 / 14%]

Household spending [everything from glue, newspapers and books to bird food, gardening stuff and parts for the bikes] – £4,076 [ 2021 £2,506] This is much higher than 2021 so was 2022 the year of stuff? There were a number of replacements; new curtains for the living room; a couple of new electronic gadgets as thngs broke and a massive frugal fail – the decision in January to buy our first tumble drier! Doing this just as energy prices were rising was pretty stupid and [of course] we hardly dare use it now. Our local library has helped us be more frugal when it comes to reading. Once I had discovered the online reservation service [75p per item] and gained my reward card [6th book free] I was hooked. Other books come from friends, charity and second-hand book shops.

Clothes & accessories – £643 [2021 £664] – We try and follow a one-in-one-out policy with clothes as even good quality kit eventually wear out and almost half of this £643 went on footwear. After putting up with wet feet time and time again on our hill walks we splashed out on a new pair of boots for me and had to replace other shoes. A massive frugal fail occured on our trip to Scotland in March. We set off in glorious and warm spring weather and forgot to pack our thick padded coats! Of course, you guessed it, a week in and the Scottish weather was Arctic and every charity shop had sold all its stock of warm and showerproof outerwear. We had no choice but to buy a coat each and were just grateful that we caught the sales. The only bonus to spending an unnecessary £130 is that we now keep these two spare coats in the campervan, so we’ll never be caught out again!

Experiences – £11,805 [46% of total spending] [2021 £9,517 / 31%]

Holidays [still our favourite spending line] – £4,096 [20210 £3,634] – We eventually got our holiday with friends in a big Scottish house in 2022, having waited two years and a pandemic to get together. We spent about four months of the year sleeping in our campervan in the UK and Germany and the Netherlands and so paid for lots of campsites and ferries but to save money we only took one trip across to mainland Europe instead of the two each year we planned when we retired.

Restaurants & cafes – £2,311 [2021 £2,225] – This number tell a story of someone who, although they love their family and friends dearly, has lost the need to socialise so much since being locked down. Our spending on eating out [everything from takeaway chips from our local chip shop to a posh meal out with friends] hasn’t recovered since BC[Before Covid-19]. In 2019 we spent just over £2,400 in this line of our budget, revealing how our life has changed and I don’t know if going out will ever return to BC levels. That said, we ate so much cake and ice-cream in Germany I’m honestly amazed this figure isn’t double!

Running the campervan [servicing & insurance etc] – £2,058 [2021 £1,280] – After a cheap year in 2021 it was inevitable we would have to spend more on the Blue Bus in 2022. The biggest expenditure was front tyres that were replaced in the autumn as they were getting to the end of their life. As the spare tyre was five years old we swapped it for one of the removed front tyres that still had some tread and a couple of years of life left in it.

Diesel for the above ‘van – £1,905 [2021 £1,261 ] – It is not surprising this budget line has increased in 2022 as the cost of diesel rocketed. Paying more than £100 to fill up its huge tank is no longer a novelty! When we are at home and on campsites we generally travel on foot, by bicycle or by public transport and our campervan can easily sit for a week or two without going anywhere. We also deliberately reduced our mileage on our trip to Europe, staying in Germany and not following the Elbe into Czechia as we had originally planned.

Tickets for concerts, football & attractions – £744 [2021 £589] – This is another area of spending that hasn’t recovered in the AC [After Covid-19] world. In 2019 we spent £200 more on going out than we did in 2022 and in 2018 we spent even more! Nevertheless we are getting back into the swing of enjoying some experiences. Gigs in 2022 included The Pretty Reckless in Manchester and we had a nostalgic trip to see Preston North End play football with a friend [we were regulars when we lived in Preston]. I sat next to a couple who had been attending PNE matches for over seven decades, what dedication! We have also visited some wonderful places, a highlight being Eilean Bàn early in the year. This island sitting under the bridge between the Isle of Skye and Kyle of Lochalsh is a haven for nature and has a delightful museum to Gavin Maxwell who lived here at one time.

Public transport costs – £691 [2021 £528] – Bus and train fares have increased. On our regular trips to Manchester to see friends we always choose to let the train take the strain but the West Coast Mainline now resembles a lottery more than a service. Three train companies run this route, Northern, TransPennine and Avanti and all of them [but particularly the latter two] have failed to provide a full timetable throughout the year even before strikes began. We now expect cancelled trains on the reduced timetable and plan accordingly after a couple of frustrating and uncomfortable journeys.

Giving – £940 [4% of total spending] [2021 £1,352 / 6%]

Gifts & donations – £940 [2021 £1,352] – In 2022 we have supported Morecambe’s Food Bank, charities campaigning against climate change and Ukraine. Whereas our donations to charities have increased, our gift giving has been more frugal. What isn’t included in this figure is the regular item I pop into the Food Bank bin in the supermarket. This is a small part of our grocery total and we find it is a way of giving without noticing the financial cost.

TOTAL SPENDING FOR 2022 – £26,405

Considering inflation and some big frugal fails I am happy with this figure. The area I would like to reduce in 2023 is the £4,700+ we spent on stuff. Even though where possible we bought second hand, much of this spending has a negative impact on our planet.

Over my six years of retirement we have spent an average of £24,715 a year.Thanks to my travel writing income over these years we have enough flexibility to be able to have a budget of more than £27,000 in 2023 and beyond without being forced to go back to the nine-to-five.

We now have only three years until we are both receiving our state pensions and no longer rely on our savings.

Although retiring early was fantastic, for me, saving was never just about being able to give up work before we were in our mid-60s, it was also about us having the financial resilience to survive whatever ups and downs life threw at us. Let’s hope we continue to stay afloat and even thrive through whatever 2023 brings us.

Let me know in the comments below how your budget matched your spending in 2022.

The clock on the oven says 3.34 as I walk carefully heel-toe, heel-toe off the wooden floor boards of our kitchen and onto the vinyl tiles of the hallway. I pass our bedroom, where my partner fortunately sleeps soundly and step onto the thick carpet of our spare room / study. There is no traffic on our dark and quiet road but I can see lights in the house across the way. The neighbour here has oxygen cylinders delivered and receives daily visits from the District Nurse and I remind myself that whatever pain I am in at this unsociable hour, there are others much worse off.

As I skirt the corner of the hallway and onto the striped and sligthly textured living room carpet I calculate how many of these nighttime walks I have done since I mysteriously did something to my lower back near the end of September when we were in Norfolk. The discomfort in my back developed into cramp-like pains down the back of my right leg that spasmed from the top of the thigh to my ankle. Within a few days this pain was waking me up at night.

I walk back along the hallway into the kitchen making sure every step counts. It is now 3.36, two minutes to complete one circuit of our small house and it only takes that long if I carefully take in all the corners. Sometimes I skip a section and then the oven clock has only moved on one minute since my last kitchen visit! There are not many times when I wish we lived in a bigger house but these night-time walks would be more interesting in a mansion and when we are away in our campervan I am basically walking on the spot!

I watch a neighbouring black and white cat saunter across our back garden before walking back down the hallway for another tour. I have found it takes at least ten minutes for the acute pain down the back of my leg to ease to something more bearable. Although the urge to go back to bed is strong, I make myself walk around for about twenty minutes before I return to my duvet. I hope my body will reward my self-restraint by allowing me a further three or four hours sleep but sometimes life isn’t like that and I am up again two hours later.

I have said before that to keep to our budget we always have some thinking time before we spend money. This might be a couple of days, a week or a month, depending on how many £s we plan to spend, but this rule goes out of the window when it comes to needing physiotherapy. You can get physiotherapy on the NHS but by the time you’ve reached the top of the waiting list your symptoms will either have gone away [a win I guess] or have become chronic and take longer to sort out. Keeping active is important to most people and I know we are lucky to have enough flexibility in our budget to spend the £55 per session for physio and for me, being able to choose what we spend our money on is an important aspect of financial independence.

The physiotherapist found an issue with my lower back and deduced that this had led to over-use of my piriformis muscle. This muscle in your hips is close to the sciatic nerve that runs down the back of the leg and if it becomes inflammed it can compress the sciatic nerve and cause pain.

For the last six weeks standing up is the only time I have a chance of being pain free and I now have breakfast standing up, I work standing up and occasionally watch television standing up. I try not to feel sorry for myself and don’t want to put my life on hold so, despite the pain, I have continued to walk and cycle. I am sure being upright during the day so much is good for me but I sometimes long to slob out for a while. I dream of curling up in an armchair with a book or kicking off my shoes, putting my feet up and watching a favourite programme. Instead, when I do sit down it is a brief moment with my back straight and supported.

But it is a full night’s sleep that I miss most. I pretty much always fall asleep easily but within a week of the initial injury I began waking in the dead of night with super-cramp down my right leg. There are plenty of suggestions for relief on the internet and I have absorbed these and shifted position and tried pillows in all the right places but frustratingly the only thing that helps a little is a heat mat [like a small electric blanket]. As every toss and turn is agony I am resigned to lying still and hoping I get at least four hours shut-eye before my brain can take no more pain and nudges me awake. No stretches or bed-based exercises give me relief and I know that walking is the only thing to do. Getting up takes effort and there are times when the pain is so intense for the first minute or so of moving around that the blood rushes from my head and I am at risk of fainting. I can’t put my head between my legs [I can hardly do up my shoe laces!] so I end up on the floor until it passes.

Some miracle manipulation by the physio that was worth every penny gave me a break from the night-time pain session for a couple of weeks in October but this has now worn off. This last week I can once again be seen, an exhausted and pathetic figure huddled in my fleecy dressing gown slowly making my way around our small house.

The frugal part of my brain had jumped at the chance to save money when, at my last appointment, the physio suggested I was doing so well I didn’t need to return for three weeks. Of course, this is a decision I am now regretting and my next session cannot come soon enough! Fingers crossed this is a temporary set back and I will soon be once again having long and sweet dreams until dawn.

As the last of our savings accounts with an interest rate over 1% matures and the cost of living in the UK keeps on rising, I have been checking out our financial position. We are all a product of our past experiences in some way and for me various life lessons put me on a purposeful and cautious journey to financial independence and early retirement [FIRE]. This journey did not involve taking risks with money; secure savings, rather than investment, was our mantra as we worked towards a goal. The FIRE community is packed with people that gainfully invest their money but my own seven life lessons led me to saving in building societies, Individual Savings Accounts and other yawningly dull and dependable accounts.

Lesson One: A broken washing machine

In my early twenties I lived on my own in a rented house, only ever one pay day away from destitution. Life improved when we got married in so many ways, including financially, but still for the first three years we muddled along with below average income and nothing in the savings pot. Then the second-hand washing machine we had inherited from a relative died. Annoying at the best of times, this felt catastrophic while we still had a child in nappies. Even in the 1980s we were environmentally conscious and we used washable and reusable cloth terry squares for our baby and dried these on the line [no tumble drier]. Washing nappies by hand was tough and it was an anxious few weeks until we managed to borrow the £250 we needed to buy a new washing machine.

Not wanting to be in that situation again the washing machine savings fund came into being. We did without and built up and kept £300 in a savings account for the next twenty years or so [long after we were washing nappies] as a security blanket.

Lesson Two: Campervans are fun!

Back in 2005 we made the life-changing purchase of our first blue campervan. Nothing was ever the same again and by the following year we knew we wanted to have a campervan gap year. Saving for this went way beyond the washing machine fund; this was big!

By 2005 we were both earning UK average salaries, our mortgage was small, our son was grown and would soon be finishing university and borrowing to buy a second-hand campervan became possible. This loan was paid off when I received redundancy pay the following year and we extended the mortgage for campervan number two. I took on multiple jobs and we became extreme savers with a clear goal to have a gap year. In the first of many spreadsheets, I began tracking our spending and savings from earnings and Ebay sales as we de-cluttered.

Lesson Three: A grown-up gap year

Having squirrelled away as much money as we thought we needed, we waved farewell to England in the spring of 2009. Our year travelling in our second blue campervan was fantastic and another huge life-changing event. We returned to Salford in 2010 having learned that early retirement was the only way we could have the freedom to travel we yearned for. We came up with a plan, secured new jobs and embarked on an even bigger saving journey with steely determination and an even more elaborate spreadsheet. Our single goal was to retire as soon as we could afford to.

Lesson Four: Banks are not always secure

We have avoided the ‘big banks’ since becoming aware of their role in debt and poverty in the global south in the 1980s. Despite the fashion for demutualisation of building societies a few remain and these are where we put our money. Although the failure of Northern Rock in 2008 only affected us lightly it did result in a ramping up of my cautiousness. Building societies are not squeaky clean but we are more comfortable with their structure and ethos. From 2010 until 2017 our ever-growing savings pots were recorded on those increasingly complex spreadsheets as we sought out the best interest rates in building societies, the government savings bank NS&I and the Co-operative Bank, spreading our cash around to limit the risk. We had a long-term plan and could tie-up money for many years and this allowed us to take advantage of reasonable interest rates.

Lesson Five: The cost of living increases

To anyone who was around in the 1970s and 80s, inflation is nothing new. With almost five years of retirement behind us the savings pots are decreasing. Now that inflation in the UK is officially over 5% and rising and our money earning little interest, we are losing value big time. I like to think savers should be able to expect their savings to ‘earn’ at least as much as inflation, staying steady rather than taking steps backwards but I have had to tweak the spreadsheet and budget to reflect these losses.

Fortunately for us this loss isn’t catastrophic as we have spent under our budget for four of the five years since we finished work. We hope that this surplus, along with my ad-hoc travel writing earnings over these years [never included in the budget] have left us with enough wiggle room to cope with an increasingly uncertain future but it does depend how bad it gets.

Lesson Six: Everyone deserves a home

Investing in housing has been popular in the UK and seen as a safe way of increasing the value of your money. Once we had sufficient funds to cover our spending for the years until our pensions paid out we could have used our savings to purchase one or two houses and become landlords, using the rent as our income. Getting our own buy-to-let might have been a wise investment decision but being a landlord is not who we are. Everyone deserves a house that feels like home and yet in my working life with homeless and vulnerable people I have learnt that many people don’t have that security. The UK’s enthusiasm for housing as an investment has inflated prices, excluded first-time buyers from the housing market and skewed the type of new properties built. I am grateful for the riches I have and count my blessings that I have a home, I am not greedy for more.

We have also never maximised the profit on our housing by pushing ourselves to have a big and bigger mortgage. We purchased our first home when we married in the mid-1980s for £13,500. The purchase was completed the day before our wedding day and with the energy of youth we married in the morning and moved across the country in the afternoon, waving to our two dozen guests from a hired Luton van full of our sticks of furniture! The small terraced house was affordable [our household income was around £6,000/year], comfortable and occasionally a headache but it was never an investment.

Moving north, we stayed in our Lancashire semi-detached house for over 20 years. To ‘maximise’ our ‘investment’ we could have taken advantage of our higher incomes and moved to a more expensive property as we reached our 40s. Our home was in the cheap-end of town but we liked where we lived and the mortgage was affordable, allowing us to enjoy a good quality of life. We still benefitted from the exorbitant rise in house prices when we sold it but by not actively playing the housing-market game and staying in a ‘cheap’ house we are now locked into the lower end of the housing market.

Lesson Seven: Sell, sell, sell

In the 1980s the Conservative government sold and privatised companies that I thought I already owned. We didn’t buy any of these get-rich-quick shares for utility companies but watching the scramble for a fast buck we added company shares into the best-avoided category.

I am clearly risk averse but in the 1980s I learnt that these investments were considered a route to wealth. We have saved to secure sufficient funds to be able to walk away from the straight-jacket of nine-to-five working and travel. Although I understand that by many people’s standards we are rich, I have never aspired to be wealthy and our money is diminishing rather than growing, as we work towards leaving this world with little or nothing.

Being comfortable with your own financial decisions

I guess if you want to free yourself from the necessity of employment in your 30s and 40s, you need firstly a high income and secondly you need to invest and achieve interest rates higher than inflation. Everyone makes their own choices, based on their life experiences and my own life lessons have left me valuing my good fortune and hesitant to squander that good fortune through risky behaviour. Fairness underpins everything we do and I hope I don’t lose sight of how lucky we are to have enough money to make choices about how we spend it.

It is the start of another year and time to share how much money we have spent in the last 12 months, revealing our spending habits in all of their immoderation. I divulge our expenditure for interest and accountability, as we aim to stay within the budget we set when we retired in 2017. Our spending is peculiar to us and comparisons are not always helpful but it does show you don’t need gold-plated pensions to have a good time. Any comments and observations are gladly received.

In 2017 we aimed to live on less than £27,000 a year for the foreseeable future and despite high inflation we spent under that figure for the fifth year running. In 2017, as new retirees, it was a generous amount for us that was around the average UK household spending but was less than we had spent while we were working. Although we had been tracking our spending for years, we didn’t really know how our retirement spending would pan out and, of course, as two vegetarians with no mortgage and a campervan there is nothing average about us! In 2020 we almost spent £27,000 but then there was nothing normal about 2020. In 2021 life was still strange but I am pleased that we have spent a comfortable £4,000+ below our budget. Our annual spending has tended to be a rollercoaster, with expensive years followed by frugal years and this trend, although it makes little sense, has continued.

As in previous years, expensive home improvements that we consider one-off are kept separate and not part of the headline figure. On top of the budgeted expenditure in the usual categories [see below], in 2021 we also spent £2,780 on new garage doors and a living room carpet. Even if this was included we would still have spent under £27,000, so I feel we have done pretty well. Our home improvements spending would have been more and we would have replaced our faded bathroom by now but have you tried getting a bathroom fitter recently?

Here is how our budget breaks down into my different categories:

Essentials – total £8,730 [38% of total spending] [2020 £9,833 / 38%]

Food – £4,142 [2020 £4,703] – We all know that prices have gone up in 2021 so I have closely monitored this spending line through the year and I am surprised it is lower than 2020. We continue to use discount supermarkets for the majority of our shopping and generally cook from scratch. The figures don’t lie and our supermarket spending seems to be inversely related to how much we spend in cafes and restaurants. In 2020 we hardly ate out at all and so food prepared at home was a bigger chunk of our costs. In 2021 we have spent more eating out so I suppose we could expect to spend less in our local supermarkets.

Utilities, insurance & service charges for a 2-bed 57.2 sq mtrs [615.7 sq feet] bungalow – £3,854 [2020 £4,463] – I am also pleasantly surprised that we spent less on our bills in 2021 than 2020 but there is an explanation that isn’t totally about being frugal. We now have two full years in the bungalow to compare our spending on this essentials category. In 2020 some bills were initially more as providers got used to the amount we would use, not realising how frugal we are! For example, our water bills started off at over £30 a month and have now settled down to £18 a month, a better reflection of what we use. We also paid more in Council Tax in 2020 as we had a few months when we didn’t pay anything in 2019 after moving. The January to April lockdown meant that we were home all the time, not something we would expect to do in a normal year. As soon as we were able we were away from mid-April to the end of June and so using no water or energy at home. We did manage to trim some of our bills in 2021 finding better deals for our mobile phones and our boiler servicing contract. In addition we complained to our previous boiler servicing company [British Gas] and received compensation after some shoddy service.

Our health [including tai chi classes] – £734 [2020 £667] – In lockdown we paid for some online tai chi classes to support our teacher and keep us healthy. In person classes re-started in September and we have attended when we can. Most of this money has been spent on new prescription specs and dental check ups.

The money we spend on the essentials above are, in theory, the minimum we need to survive, if nothing goes wrong or wears out and we didn’t own a campervan and never went anywhere!

Stuff (electronics, books, newspapers and other kit) – £3,170 [14% of total spending] [2020 £7,175 / 27%]

Household spending [everything from glue, newspapers and books to bird food, gardening stuff and parts for the bikes] – £2,506 [ 2020£6,189] 2020 was the year of DIY! 2021 has been more about getting out and about. When we do buy furniture we continue to try and buy second-hand and in 2021 we have sourced some fabulous items that will last the rest of our lifetimes. It is hard to call the G-Plan large chest of drawers a bargain at just under £200 but they are beautifully made and the drawers glide in place. A second-hand wine rack and a small cupboard were other good buys from our local GB Antiques emporium. We search out second-hand books in charity shops and the warren-like Pier Bookshop in Morecambe and, even better, when we can we borrow books from our local library for free!

Clothes & accessories – £664 [2020 £986] – Again, I am pleased we haven’t spent more in this category. There have been a couple of essential purchases. My partner wore his hiking boots up lots of hills but eventually the sole lost contact with the body of the boot. Some glue kept them together during our holiday in Ireland but we did have to purchase more this summer. We both also needed new walking shoes and after mine caused massive blisters and bruising on my feet I complained to the manufacturer. They sent me replacement shoes but I am not convinced they were faulty and think it is a design issue and I haven’t dared to wear them yet. In the meantime I had purchased a pair of Vivo Barefoot walking shoes. I love their shoes but hadn’t tried their more substantial styles before and I am really pleased with them. This palaver does mean I bought two pairs of walking shoes in 2021! More frugally, while we were in Ilkley this summer I spent some time in the excellent charity shops in this well-heeled town and purchased some good quality second hand items I needed, including a soft and floaty summery frock for a few quid that is perfect for the four or five days a year it is warm enough to wear such a thing.

Experiences – £9,517 [31% of total spending] [2020 £8,336 / 31%]

Holidays [our favourite spending line] – £3,634 [2020 £2,834] – As well as plenty of nights on campsites, other holidays are in this category. Having had so many plans disrupted in 2020, we were determined to make the most of spending time with friends in 2021 and have had a couple of lovely weekends in hotels in the Lake District. In 2019 we paid for a self-catering cottage holiday with friends in Scotland for 2020. This was obviously postponed to 2021 and, due to another lockdown, has now been postponed to 2022. Is this a record for the longest wait for a holiday?

Restaurants & cafes – £2,225 [2020 £1,309] – After a woeful 2020, our 2021 spending in this category is nearer to our 2019 spending, although we haven’t got back to the regular meet ups and meals with friends in Manchester. We did manage a sociable night at Manchester’s Christmas Market and paying a small fortune for a mug of warming gluwein felt like a massive treat!

Running the campervan [servicing & insurance etc] – £1,280 [2020 £2,093] – It has been a cheap year for the van. No doubt the Blue Bus is saving up for some expensive new parts it wants in 2022!

Diesel for the above ‘van – £1,261 [2020 £1,227 ] – We travelled to northern Scotland and across Northern Ireland to Donegal but certainly haven’t put the miles across Europe on the campervan we would normally do.

Tickets for concerts, football & attractions – £589 [2020 £403] – By the autumn of 2021 we felt ready to attend events and gigs again. We attended a Manchester Literary Festival events and saw Chantel McGregor and Turbowolf live. I have missed live music and it was so amazing to immerse myself in it again for an evening. We have been to see Morecambe FC a couple of times too, where you win some and lose some. In the spring many venues weren’t open but by the time we travelled to Wales in September we could visit a bevy of castles.

Public transport costs – £528 [2020 £360] – Most of this is the cost of going to and from Manchester by train.

Giving – £1,352 [6% of total spending] [2020 £937 / 4%]

Gifts & donations – £1,351 [2020 £937] – Another discretionary spending line that we enjoy spending but try and keep under control. In terms of donations, we have given to some favourite local and national charities throughout the year. Our gift giving has been more extravagant in 2021 due to so many disappointments in 2020. The most expensive gift was treating our son and daughter-in-law to a weekend away in a Lake District hotel. The downside for them was that we came too! Time with them is very precious and worth every penny.

TOTAL SPENDING FOR 2021 – £22,769 – I am very pleased we have kept the spending low this year and still enjoyed ourselves and will indulge in a small pat on the back!

Over my five years of retirement we have spent an average of £24,744 a year.

We are gradually spending our savings but our expenditure doesn’t all come from the money we have squirreled away. As well as my side hustle travel writing income, in 2020 my small NHS pension began. This is based on my many years of part-time and full-time NHS work and is the equivalent to 12 years NHS service. These both help to reduce what we take from the ever-diminishing savings pot.Although retiring early was fantastic, for me, saving was never just about being able to give up work before we were in our mid-60s, it was also about us having the financial resilience to survive whatever ups and downs life threw at us. Let’s hope we continue to stay afloat and thrive.

It is that time of the year again when I share how much money we have spent in the last 12 months, revealing our spending habits in all their profligacy. I divulge our expenditure for interest and accountability, as we aim to stay within a budget. Our spending is peculiar to us but any comments are gladly received.

Our budget remains at £27,000 a year for the fourth year running. This is now below the average UK household spending. The headline is that despite the strange year we have had our outgoings for 2020 came within budget [hurrah], although the headline doesn’t tell the whole story. As I said last year, our annual spending seems to go up and down like a rollercoaster, with alternating frugal years and expensive years. Sometimes it is our campervan that costs us a lot of money but 2020 was a year of home-making and healthcare.

It is just over twelve months since we moved to our Morecambe bungalow. The home improvements that are included in our 2020 spending are all things we would expect to carry out more than once in our [expected] remaining lifetime. These purchases include a new bedroom carpet to replace the grotty brown carpet from the 1980s that came with the bungalow and could tell a tale or two; new furniture to replace some that was second-hand 36 years ago, a new sofa bed [as we thought we would have visitors!] as well as smaller items like paint, varnish and brushes. More expensive home improvements which we consider one-off items are kept separate. So, on top of the budgeted expenditure in the usual categories, in 2020 we spent £13,300 on new windows and doors, resurfacing the drive and a new kitchen.

Not unsurprisingly our 2020 spending reflects the Covid-19 factor. The breakdown shows that we had less opportunities for experiences and spent more of our money on food in supermarkets and local shops.

Essentials – total £9,833 [38% of total spending] [2019 £7,721 / 35%]

Food – £4,703 [2019 £3,491] – In my experience food prices have increased in 2020 as we haven’t eaten anything different or developed an expensive taste in anything. We will have spent more as we have eaten mostly at home [sitting eating around a friend’s dining table is a distant memory]. We continue to use discount supermarkets for the majority of our shopping and generally cook from scratch.

Utilities, insurance & service charges for a 2-bed 57.2 sq mtrs [615.7 sq feet] bungalow – £4,463 [2019 £3,974] – The various lock downs and restrictive tiers mean who have been home more than ever and so using more gas and electric. Council tax and heating for the bungalow are both more expensive than the flat, but we no longer have service charges to pay. The improvements we have made to bring our bungalow into the 21st century will help save money on utilities.

Our health [including tai chi classes] – £667 [2019 £256] – There has been very little spending on tai chi classes in 2020 and this is mostly some expensive dental work and new specs.

In theory this is the minimum we need to survive a year, although it would be a strange year when we didn’t need / buy some stuff.

Stuff (electronics, newspapers and other kit) – £7,175 [27% of total spending] [2019 £3,151 / 14%]

Household spending [everything from glue, newspapers and books to hiring a sander, plants for the garden and parts for the bikes] – £6,189 [ 2019 £2,300] – Wow! We have clearly had too much time for DIY and nest building this year! In 2019 we were moving house and the only DIY we did was freshening up the paint for the sale of our flat. This is a big category, with furniture, carpet, cushions and pictures on the walls all thrown into it. I am uncomfortable buying stuff and we try and source antiques / junk / second-hand items when this is practical. Bargain purchases this year included an Edwardian What Not [yes really] for a kitchen wall to contrast with the shiny white units for £30, second-hand lined curtains for the large living room window for £25 and some second-hand cushion covers for £5.

Clothes & accessories – £986 [2019 £851] – I have never gone down the route of a clothes buying ban, preferring to stick to buying what I need, as something wears out. Pretty much all the clothes we bought in 2020 were hard-wearing hill walking kit and probably not most people’s idea of clothes shopping. I needed new boots, we bought new waterproof trousers, a fleece, wellies and some comfy walking shoes; these were all replacement items. Where we could we bought second-hand items, for example a men’s winter coat on Ebay was just £24. Even when you buy quality items they don’t last forever but our walking gear gets plenty of wear; my previous boots had walked a lot of miles over six years.

Experiences – £8,226 [31% of total spending] [2019 £10,952 / 48%]

Holidays [our favourite spending line] – £2,834 [2019 £3,601] – The reason for this reduction in our holiday spending in 2020 is obvious and it isn’t because I have lost my wanderlust! In the north-west of England we have had travel restrictions for over six months of the year. We did get away a few times in the first three months of the year before the three months of lock down. We spent July taking trips to the Lake District, got to France in August and [after quarantine] thankfully managed to travel to Scotland in October. We have also paid for a holiday in a self-catering house in Scotland that has been moved to 2021 [fingers crossed].

Restaurants & cafes – £1,309 [2019 £2,418] – Despite using local cafes and restaurants when we can this year and having more takeaways than we would normally do to support local businesses this is much lower than normal. It is not particularly the food I miss, what I have really miss is seeing friends. In a normal year there are two old friends we would meet about eight times a year for drinks and a meal at a cost of about £500. Chatting over Zoom, although cheaper, hasn’t been the same. Interestingly, the reduction in our eating out spending is more or less off-set by the increase in our food spending.

Running the campervan [servicing & insurance etc] – £2,093 [2019 £1,931] – Last year I wondered if our six year old Renault Master was saving up some expensive repairs for 2020. It hasn’t done too badly but needed some essentials like tyres and brakes replacing as well as the usual servicing, insurance and road tax.

Diesel for the above ‘van – £1,227 [2019 £1,500 ] – We certainly haven’t put the miles across Europe on the campervan we would normally do.

Tickets for concerts, football & attractions – £403 [2019 £941] – Well what do you expect as for much of the year nothing was open. Live music is just a distant memory and the last football match we went to was a Morecambe FC match last Christmas. We have supported some arts events by buying tickets for online events and visited some RSPB reserves when we could.

Public transport costs – £360 [2019 £561] – Again, the pandemic effect has kept us at home much of the time.

Giving – £937 [4% of total spending] [2019 £654 / 3%]

Gifts & donations – £937 [2019 £654] – Another discretionary spending line that we try and keep under control but in 2020 we felt a need to be more generous. Many charities needed additional funding as events and places were closed and during the first lock down we sent cheering-up parcels to friends, as well as the usual birthday and Christmas gifts.

TOTAL SPENDING FOR 2020 – £26,171 – Despite all the home-making we have done in 2020, we have stayed within our £27,000 budget.Hurrah!

Over my four years of retirement we have spent an average of £25,351 a year.

Our expenditure doesn’t all come from our savings. As well as my side hustle travel writing income [reduced in 2020 due to Covid-19], in 2020 my small NHS pension began. This is based on my many years of part-time and full-time NHS work and is the equivalent to 12 years NHS service. These both help to reduce what we take from the ever-diminishing savings pot.For me, saving for early retirement was never just about giving up work, it was also about us having the financial resilience to survive whatever ups and downs life threw at us.

2019 has been an unusual year with no trips abroad in our campervan and a house move. We have stayed alive and healthy and we spent two months touring Scotland in our campervan, learning to love that country even more and visiting Shetland for the first time, leaving a little bit of our hearts there. Financially it has been good too. We have stayed within budget; in 2019 our household spending was as low as £22,428. The ONS calculate that the average household in the north-west of England spent £26,062 a year in 2017-2018. Of course, this average will include large families and single-person households, households that have expensive hobbies [like a campervan], those who are home all day and people who have little money or are super-frugal. Although we don’t consider ourselves to be average, we generally aim to spend less than this average. I had hoped that our frugal fail in 2018 was a blip [we spent over £28,000] and it certainly seems that we have got back on track in 2019.

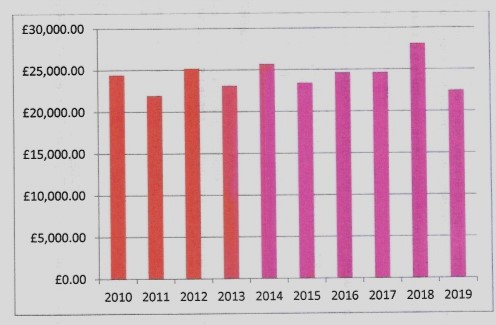

Our household spending from 2010 to 2019

Despite the rigour of my spreadsheets, our annual spending creates a graph that looks like a roller coaster and this does make a bit of a joke of the budgeting we do. Over the last nine years our spending has ranged over £6,000 from £21,972 to £28,107, not allowing for inflation. All this information really tells me is there are expensive years and cheaper years and that our budget for 2020 of around £26,000 doesn’t look too unrealistic. What is interesting is that our 2019 spending of £22,428 is our next to lowest spending year [and a rough online inflation calculator suggests that £21,972 in 2011 is now the equivalent of over £27,000] so for us 2019 has been a frugal year.

This household spending does gloss over the £36,000 plus that has disappeared from our savings and been spent on our recent house move and the improvements to bring our 1960s bungalow into the 21st century. It seemed fair to leave out these one-off costs as they would have massively skewed the figures but it also seemed best to fess up about this spending here. Of course before we took the plunge of moving we did the sums and, although when our pensions start paying in 2026 we will have considerably less savings in the bank, we felt it was an outlay that was manageable … but time will tell. The move became essential for our well-being and we are reasonably comfortable that we will have enough of an emergency fund to take us into our old age. Who knows what will happen with the cost of care by the time we are in our 80s and whether we will need any. We certainly won’t have much money spare for anything expensive but we live in hope that a fair system will be in place by then.

Our own expensive hobby of running a campervan and having lots of holidays continues and this is generally our downfall. If we never went anywhere our spending would be much lower! Everyone spends their money in their own way, this is how our 2019 spending pans out:

Essentials – total £7,721 [35% of total spending] [2018 £9,654 / 34%]

Food – £3,491 [2018 £3,870] – This is an essential but also an easy area to control and after the shock of 2018 we have been careful to use the cheaper supermarkets. We cook mostly from scratch, including making bread, only ever buy what we need and rarely waste anything. We now have a garden but don’t expect to start growing food, as this doesn’t really work with taking a long holiday.

Utilities, insurance & service charges for a 2-bed 58 sq mtrs [624 sq feet] flat for 10 months & a 2-bed 57.2 sq mtrs [615.7 sq feet] bungalow for 2 months – £3,974 [2018 £4,841] – We have been home more than previous years but try and restrain our use of the heating and water. Our bungalow is more expensive to run in terms of utilities than the flat, despite good insulation, so watch this space for 2020. But a big plus of not living in a flat is that we no longer have service charges of over £1,000/year! On the flip-side we are now responsible for the upkeep of our four walls and roof, not to mention a garden, this feels a bit daunting just at the moment.

Our health [including tai chi classes] – £256 [2018 £943] – We had no expensive spectacles or dental work this year, hurrah! We were lucky to find another reasonably priced tai chi class in Morecambe, at £3 each a week this is manageable and we can afford to attend regularly.

Stuff (electronics, newspapers and other kit) – £3,151 [14% of total spending] [2018 £3,333 / 11%]

Household spending [everything from glue and newspapers to parts for the bikes and a new kettle] & miscellaneous un-identified items – £2,300 [ 2018 £2,364] – We are a long way from a no-spend year on stuff but I’m relieved that this spending line is similar to 2018 as I thought that moving house might have spiralled this into another realm as we splashed out on new [to us] curtains, gardening equipment and a Remoska oven.

Clothes & accessories – £851 [2018 £969] – I am really pleased this spending line is lower than last year, particularly when I take into account that over half of this is accounted for by new waterproof jackets. We took a deep breath and bought quality so hope they will last for years and years – maybe until we die?

Experiences – £10,952 [48% of total spending] [2018 14.095 / 51%]

Holidays [our favourite spending line] – £3,601 [2018 £4,681] – Our holiday spending is less than other years as [thanks to the house move] we didn’t get abroad but we did spend a fantastic two months touring Scotland. Factor in the cost of the ferry to Spain in 2018 [about £900] and this line would have pretty much stayed the same; the ferries are really the biggest chunk of our holiday costs. We spent only 108 nights away in our campervan, less than previous years [again due to the house move] but campsites in the UK are often more expensive than mainland Europe. We took ourselves off for 10-days during the house buying process and returned to a pile of paperwork waiting to be signed, after that we hardly dared venture away. This does include a splash-out weekend in a swanky Lake District hotel to celebrate a significant birthday.

Restaurants & cafes – £2,418 [2018 £2,963] – This is another chunk of spending that we can keep under control if we need to but we love meeting friends for meals out and sitting in friendly cafes. So I am surprised [and pleased] this spending is lower than in 2019 as we seem to have been out with friends on plenty of occasions … but the numbers don’t lie!

Running the campervan [servicing & insurance etc] – £1,931 [2018 £2,578] – I was excited to find that moving to Morecambe from Salford reduced our insurance costs on our campervan, although it is no longer parked in a gated car park! 2018 was an expensive year for our ‘van and in 2019 we didn’t take such a hit spending £800 on fixing things on our campervan to keep it on the road. Our ‘van is almost five years old and has driven around 50,000 miles and among other things it needed new brakes and reversing sensors. I think the ‘van might be saving everything up for 2020 though!

Diesel for the above ‘van – £1,500 [2018 £1,937 ] – This is lower due to reduced campervan trips and lower mileage through the year.

Tickets for concerts, football & attractions – £941 [2018 £1,114] – A cheaper year but we have still had lots of fun experiences seeing bands, going to the football and getting face to face with a pine marten.

Transport costs included buses, trains & parking – £561 [2018 £670] – My target to walk 2,019 km in 2019 kept this number down as I was constantly choosing to walk rather than take the tram or bus. We have spent more for the last two months of the year since moving to Morecambe, as not wishing to pollute the world more than we need to we have taken the train to Manchester on all but one occasion.

Giving – £654 [3% of total spending] [2018 £1,025 / 4%]

Gifts & donations – £654 [2018 £1,025] – Another discretionary spending line and we can only hope our family and friends understand why presents, although still thoughtful, have been small in 2019.

TOTAL SPENDING FOR 2019 – £22,478 – staying comfortably within our £26,000 budget helps to give us some financial resilience for future years.

1986 seems like another era; I had big hair, we owned a British Leyland Metro, Spitting Image was still on TV and we moved to Preston in Lancashire. Along with fashions, the pattern of the communities in our cities have also altered many times since those days. As a young couple with a tiny baby and two cats, living away from our home town and our respective families, we moved into a 19th century brick-built terraced house in a row of similar terraced houses. This was our stomping ground for two years before we became upwardly mobile and moved to a more spacious semi-detached house.

These Lancashire terraced streets are still there and continue to provide great housing for families. Our small terrace had two downstairs rooms and upstairs a double bedroom, two single bedrooms and a small bathroom. Along the side of the house was a narrow alley that went underneath our upstairs rooms and that we shared with our neighbour. This gave us access to the back yard and garden and was where we stored ladders and bikes.

In the 1980s we weren’t on our journey to financial independence, our priority was keeping our heads above water. We were a single-income family with a mortgage on a house that had cost us £15,000 [you now need almost this much for a deposit on these properties]. Our terraced row of houses felt crowded but comfortable. Along with our neighbours, none of us were wealthy; here was the wonderful diversity of what might be called the working classes, all struggling to make ends meet. Although our family income came from a ‘professional’ job at the university, this is where we could afford to live.

To one side lived a couple with one child. He had worked as a jockey, riding horses, as a young man but was now a butcher, both fascinating worlds I knew little about. She was an outgoing hairdresser, working in a city centre salon. On her day off she styled the hair of the neighbours in their homes, including me, giving us mates rates. While we lived next door their marriage broke down and she began working evenings in a Preston nightclub for extra income as a pole dancer, another world I knew little about.

To our other side lived a couple with two children, a family living on the single income of his manual job. It was this mum that was usually the parent that would offer to sit on the front step and watch her own children play in the street during the early evening, along with those of neighbours. If the weather was fine I would often join her for a while with the baby and sitting on our respective steps we would talk generally about family news, the best schools and favourite TV programmes. It was on these steps that I was informed that the best local primary school was the Roman Catholic school; I mentioned that we were atheists but she didn’t really grasp why that would mean this school wasn’t suitable for our little one.

During the daytime the street was a place for women and young children, all the men were at work and my early lessons in bringing up a child came from these women. The street was lived in by families that were white-British but we were on the edges of more diverse areas of Preston and nearby there were shops that sold exotic fruit and vegetables that I enjoyed exploring. At the end of the street, in the 20th century social housing, was a Muslim woman with children. She was divorced, somewhat unusual in her community, and this single status sadly led to bullying by people who shared her religion; she needed a friend and sometimes I listened.

Just around the corner were an elderly couple, long-time residents of the area. On warm afternoons he liked to bring a dining chair outside his tiny two-up-two-down terraced house and sit and chat to anyone who came by. I walked by his house to the local shops and into town, always carrying our baby in a papoose, and would stop for a while. He told me funny and interesting stories of his days as an engineer building bridges on the M6. Life seemed to be slower in those days in this corner of Preston and people had time to talk.

Another family across the road had a son who was difficult to manage, he was often aggressive and sometimes violent. He was removed from home and sent to the local children’s home that was unfortunately just 100 metres away. He continued to return home and scream loudly outside his family home and once he broke a window while everyone along our street cowered indoors, no one trying to help. In these narrow streets there is nowhere to hide and the family’s shame was a burden they carried, knowing the next day that everyone was talking about them.

On the corner of the road was the vicarage. The vicar and his friendly wife had four children and were considered the middle-class residents of the street. Quizzing me about how many more children we would have, I told her, ‘One is enough.’ She failed to persuade me that a big family was the way to go. Their house was an enormous rambling property surrounded by a garden and easily swallowed their large family and the numerous visitors they happily entertained.

I have said before I have a literal mind and so when I learnt there was a Mums and Toddler Group nearby [these would now be called a play group or parent and toddler group] I understood the term precisely and didn’t attend until our son was actually toddling at 11 months old. I laughed when I was told I didn’t have to wait until he could walk! The group was held twice a week in a draughty and dismal church hall with a selection of old toys for the children to play with and tea and biscuits for the mums / parents. In this unpromising environment, there was no sense of competitive parenting and everyone was supportive and helpful and I learnt more child-rearing skills. It was here that I met parents who shared my love of reading, cooking good food, an interest in environmentalism and fellow atheists who recommended the local county primary school. I made some firm friends here and the plan to move a short distance away to a bigger house began.

The narrow terraced streets are still there and probably still lived in by hard-working families. The vicar no longer lives at the end of the road and the extensive garden is now a car park, the social housing has been improved. The corner shop has gone, along with the telephone box where we would ring distant family and friends as we didn’t have a home phone. Traffic has increased everywhere and I doubt if I walked here on a sunny evening I would still see parents sitting on the steps watching their children playing in the street but then again …

In 2017 I was feeling a trifle smug. We had spent around £24,000 in our first year of retirement, way below budget. That smug smile was wiped off my face earlier in the year when I reported that things were not looking so positive in 2018 and I was feeling a frugal failure. With inflation I could have expected our spending to increase to around £25,000 in the year, instead it seems we were just saving up all our big financial hits for 2018. In 2018 we were just average [2017 UK average household spending was £28,818). This isn’t much comfort when we’re supposed to be being frugal and minimalist. In our spending you won’t find any costs for haircuts, party frocks, frippery or pay TV, so what went wrong? I’ve divided our spending this year in to essentials, stuff, experiences and giving. The graph gives a summary.

Essentials – total £9,654 [34% of total spending]

Food – £3,870 – We are two vegetarian who like to drink red wine and gin & mostly use the discount supermarkets. I do know that wine and gin are not essential but we haven’t separated the costs of these from our supermarket shops during the year and together these probably represent about £400 of the total. [2017 £3,612]

Utilities, insurance & service charges for a 2-bed 58 sq mtrs [624 sq feet] flat – £4,841 – This year we have changed supplier for our gas and electric and moved to a cheaper mobile phone contract to save money. The increase is only because we payed up-front for the gas boiler servicing to receive a discount [2017 £4,621 mis-reported last year!]

Our health [including tai chi classes [?essential?]] – £943 – An expensive year thanks to some dental work [£235] and both of us needing new specs [£503] [2017 £376]

Stuff (electronics, newspapers and other kit) – £3,333 [11% of total spending]

Household items [including parts for the bikes] – £2,364 – Although this category does include a multitude of things, including postage, one newspaper a week, books [often second-hand] and bits and bobs for repairs, it also includes stuff. In 2018 we decided to buy a new laptop [£450] and one new mobile phone [£115], replace our ageing head torches [£70] and cycle helmets [£50]; although all replacing old and well-used items these are purchases that we don’t make easily and we had been putting off for some time. [2017 £1,668]

Clothes & accessories – £969 – Whenever we can we buy second-hand clothing. The almost £1,000 we have spent is mostly for replacements for walking gear that has worn out. Even with the best quality clothing things don’t last forever and this year we have bought new walking shoes, trousers and rucksacks. It is true that about £100 of this spending is for a couple of things that were bought because of a want, rather than a need. [2017 £525]

Experiences – £14,095 [51% of total spending]

Holidays [our favourite spending line] – £4,681 – Despite being away on holiday for even longer, around 40% of the year [155 nights in the campervan, plus a couple of other holidays in self-catering cottages] we have spent less on this budget line in 2018. Result! The spending is mostly on accommodation and ferries and also includes £380 for a 2019 holiday. [2017 £5,285]

Restaurants & cafes – £2,963 – Only a tad more than last year [2017 £2,864]

Running the campervan [servicing, insurance & parts] – £2,578 – a big increase on last year [2017 £1,636] all due to replacing brakes and tyres, failures in the air conditioning and power steering and a bit of wing mirror jousting. What a year! Readers might not agree that the costs for our campervan come under experiences but for us this is an important part of our lifestyle and so this is where it fits best. Friends might be surprised that I didn’t put it under essential spending!

Diesel for the above ‘van – £1,937 – the price of diesel has increased and we drove more miles in the Blue Bus this year, particularly on our trip to Croatia[2017 £1,641]

Tickets for concerts, football & attractions – £1,114 – Wow! We must have been to a lot of events this year! Tickets for the football have increased in price and in Croatia we visited more paying attractions than we might have as we’re unsure whether we will travel so far again. Although this is experiences, rather than stuff, this is definitely an area we could try and make savings in 2019. [2017 £633]

Public transport – £670 – We don’t use the campervan around Manchester and cycle and walk to do things or visit friends but sometimes [if it is raining/cold/too far] we take the tram, the bus or the train [2017 £517]

Unknown spending – £152 – [2017 £81]

Giving – £1,025 [4% of total spending]

Gifts & donations – £1,025 – we buy our family and friends birthday presents and buy Christmas presents for a shorter list [2017 £1,173]

TOTAL SPENDING FOR 2018 – £28,107 [2017 £24,196]

I’m pleased to see how much our spending is weighted towards doing things, rather than buying stuff so perhaps a tick for being minimalist if not uber-frugal. Despite having a year that has still been a bit heavy on replacing things 51% of our spending has been on our own version of enjoying life. We have a plan to cut down our spending on stuff in 2019 and I hope spending only 4% on giving make us look frugal rather than mean as I’d like this to remain this low.

It is impossible to make any conclusions from one year and averaged over two years our spending of £26,152 a year still seems fairly low. This year has shown us how important over-saving or over-estimating budgets is for planning to live without any earned income. After this expensive year my travel writing income is becoming essential, rather than extra cash.

Having spent more than our original budget of £27,000 our future annual budgets have been increased to reflect this. We’ll see what 2019 will bring and try hard to have a low-spending year but at the moment we have no need or plans to go back to the nine-to-five!